Consolidation Entries Statement Assignment

- Country :

Australia

Jonathan Ltd acquired all the issued shares (ex-div.) of Thomas Ltd on 1 July 2020 for $246 000. At this date the equity of Thomas Ltd consisted of:

Share Capital= $130,000

General Reserve=$50,000

Retained Earnings= $50,000

At the acquisition date all the identifiable assets and liabilities of Thomas Ltd consisted of:

| Carrying Amount | Fair Value | |

|---|---|---|

| Plant (Cost $230,000) | $200,000 | $210,000 |

| Land | $100,000 | $120,000 |

| Inventories | $30,000 | $38,000 |

The inventories were all sold by 30 June 2020. The land was sold on 1 February 2021 for $150 000. The plant was considered to have a further 5-year life. The plant was sold for $155 000 on 1 January 2022. Also, at acquisition date Thomas Ltd had recorded a dividend payable of $7000 and goodwill (net of accumulated impairment losses of $13 000) of $5000. Thomas Ltd had not recorded some internally generated brands that Jonathan Ltd considered to have a fair value of $12 000. The brand was considered to have an indefinite life. Also not recorded by Thomas Ltd was a contingent liability relating to a current court case in which Thomas Ltd was involved and a supplier was seeking compensation. Jonathan Ltd placed a fair value of $15 000 on this liability. This court case was settled in May 2022 at which time Thomas Ltd was required to pay damages of $16 000.

In February 2021, Thomas Ltd transferred $20 000 from the general reserve on hand at 1 July 2020 to retained earnings. A further $15 000 was transferred in February 2022.

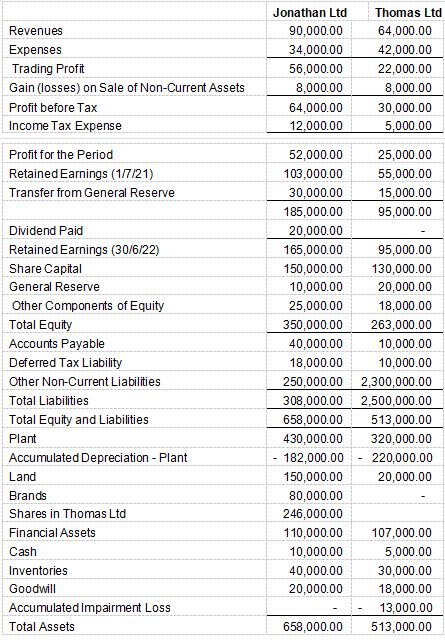

Both companies have an equity account entitled 'Other components of equity' to which certain gains and losses from financial assets are taken. At 1 July 2021, the balances of these accounts were $30 000 (Jonathan Ltd) and $15 000 (Thomas Ltd). The financial statements of the two companies at 30 June 2022 contained the following information:

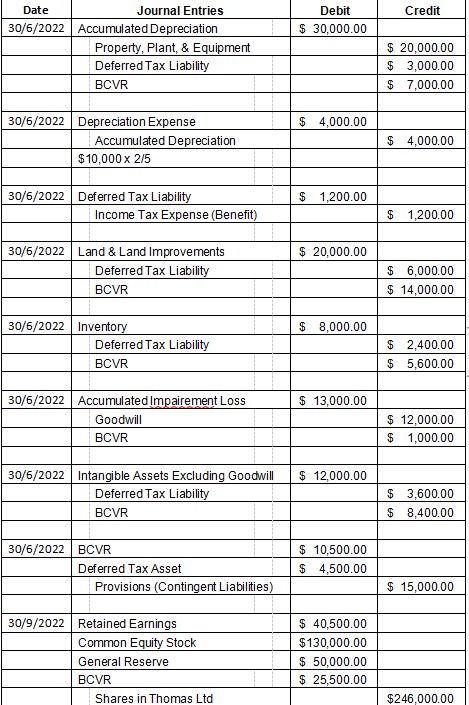

- Calculate acquisition analysis as at 1 July 2020.

Net Fair Value of Identifiable Assets & Liabilities of Thomas Ltd = ($130,000 + $50,000 + $40,500) (equity) + $8,000 (1 30%) (inventory) + $10,000 (1 30%) (plant) + $20,000 (1 30%) (land) + $12,000 (1 30%) (internally generated brand) - $15,000 (1 30%) (provision for damages) - $5,000 (goodwill) = $220,500 + $5,600 + $7,000 + $14,000 + $8,400 - $10,500 - $5000 = $240,000

Consideration transferred = $246,000

Goodwill = $246,000 - $240,000 = $6,000

Goodwill Recorded = $5,000

Unrecorded Goodwill = $1,000 - Prepare the consolidation journal entries for 30 June 2022.

- Complete the consolidated worksheet for 30 June 2022

- Prepare the consolidated financial statements at 30 June 2022

- Write a report to explain the consolidation process as per AASB10 for wholly owned entities.