Financial Markets and Institutions FIN3004

- Subject Code :

FIN3004

DIDSECURITIZATIONLEADTOLAXSCREENING?

EVIDENCEFROMSUBPRIMELOANS?

Benjamin J. Keys TanmoyMukherjee Amit Seru

VikrantVig

A central question surrounding the current subprime crisis is whether the se-curitization process reduced the incentives of financial intermediaries to carefullyscreen borrowers. We examine this issue empirically using data on securitizedsubprimemortgageloancontractsintheUnitedStates.Weexploitaspecificruleof thumbin the lending market to generate exogenous variation in the ease ofsecuritizationandcomparethecompositionandperformanceoflendersportfoliosaround thead hocthreshold. Conditional on being securitized, the portfolio withgreater ease of securitization defaults by around 10%25% more than a similarrisk profile group with a lesser ease of securitization. We conduct additional anal-yses to rule out differential selection by market participants around the thresholdand lenders employing an optimal screening cutoff unrelated to securitization asalternative explanations. The results are confined to loans where intermediariesscreening effort may be relevant and soft information about borrowers determinestheir creditworthiness. Our findings suggest that existing securitization practicesdidadversely affect the screening incentives of subprime lenders.

- Introduction

Securitization, converting illiquid assets into liquid securi- ties,hasgrowntremendouslyinrecentyears,withtheuniverse ofsecuritizedmortgageloansreaching$3.6trillionin2006.The?We thank Viral Acharya, Effi Benmelech, Patrick Bolton, DanielBergstresser,CharlesCalomiris,DouglasDiamond,JohnDiNardo,CharlesGood-hart, Edward Glaeser, Dwight Jaffee, Chris James, Anil Kashyap, Jose Liberti,Gregor Matvos, Chris Mayer, Donald Morgan, Adair Morse, Daniel Paravisini,KarenPence,GuillaumePlantin,ManjuPuri,MitchPetersen,RaghuramRa-jan, Uday Rajan, Adriano Rampini, Joshua Rauh, Chester Spatt, Steve Schaefer,Henri Servaes, Morten Sorensen, Jeremy Stein, James Vickery, Annette Vissing-Jorgensen, Paul Willen, three anonymous referees, and seminar participants atBoston College, Columbia Law, Duke, the Federal Reserve Bank of Philadel-phia, the Federal Reserve Board of Governors, the London Business School, theLondon School of Economics, Michigan State, NYU Law, Northwestern, Oxford,Princeton, Standard and Poors, the University of Chicago Applied EconomicsLunch, and the University of Chicago Finance Lunch for useful discussions. Wealso thank numerous conference participants for their comments. Seru thanksthe Initiative on Global Markets at the University of Chicago for financial sup-port. The opinions expressed in the paper are those of the authors and do notreflect the views of the Board of Governors of the Federal Reserve System orSorin Capital Management. Shu Zhang provided excellent research assistance.Allremainingerrorsareourresponsibility.benjamin.j.keys@frb.gov,tmukherjee@sorincapital.com,amit.seru@chicagogsb.edu,vvig@london.edu.

?C2010bythePresidentandFellowsofHarvardCollegeandtheMassachusettsInstituteofTechnology.

TheQuarterlyJournalofEconomics,February2010

307

option to sell loans to investors has transformed the traditional role of financial intermediaries in the mortgage market from buy- ingandholdingtobuyingandselling.Theperceivedbenefits of this financial innovation, such as improving risk sharing and reducing banks cost of capital, are widely cited (e.g., Pennacchi [1988]). However, delinquencies in the heavily securitized sub- primehousingmarketincreasedby50%from2005to2007,forcing manymortgagelendersoutofbusinessandsettingoffawaveoffi- nancial crises, which spread worldwide. In light of the central role ofthesubprimemortgagemarketinthecurrentcrisis,critiques of the securitization process have gained increased prominence (Blinder 2007; Stiglitz 2007).

The rationale for concern over the originate-to-distribute model during the crisis derives from theories of financial inter- mediation. Delegating monitoring to a single lender avoids the duplication, coordination failure, and free-rider problems associ- ated with multiple lenders (Diamond 1984). However, for a lender to screen and monitor, it must be given appropriate incentives (Holmstromand Tirole 1997), and this is provided by the illiquid loans on its balance sheet (Diamond and Rajan 2003). By creating distance between a loans originator and the bearer of the loans default risk, securitization may have potentially reduced lenders incentives to carefully screen and monitor borrowers (Petersen and Rajan 2002). On the other hand, proponents of securitization argue that reputation concerns, regulatory oversight, or sufficient balance sheet risk may have prevented moral hazard on the partof lenders. What the effects of existing securitization practices on screening were thus remains an empirical question.

This paper investigates the relationship between securitiza- tion and screening standards in the context of subprime mortgage loans. The challenge in making a causal claim is the difficulty of isolatingdifferencesinloanoutcomesindependentofcontractand borrower characteristics. First, in any cross section of loans, those that are securitized may differ on observable and unobservable risk characteristics from loans that are kept on the balance sheet (not securitized). Second, in a time-series framework, simply doc- umenting a correlation between securitization rates and defaults may be insufficient. This inference relies on establishing the opti- mal level of defaults at any given point in time. Moreover, this ap- proach ignores macroeconomic factors and policy initiatives that may be independent of lax screening and yet may induce composi- tional differences in mortgage borrowers over time. For instance,

house price appreciation and the changing role of government- sponsored enterprises (GSEs) in the subprime market may also haveacceleratedthetrendtowardoriginatingmortgagestoriskier borrowers in exchange for higher payments.

Weovercomethesechallengesbyexploitingaspecificruleofthumbinthelendingmarketthatinducesexogenousvariationin theeaseofsecuritizationofaloancomparedtoanotherloanwith similar observable characteristics. Thisrule of thumbis based on the summary measure of borrower credit quality known as theFICOscore.Sincethemid-1990s,theFICOscorehasbecome the credit indicator most widely used by lenders, rating agen- cies, and investors. Underwriting guidelines established by the GSEs, Fannie Mae and Freddie Mac, standardized purchases of lenders mortgage loans. These guidelines cautioned against lend-ingtoriskyborrowers,themostprominentruleofthumbbeing not lending to borrowers with FICO scores below 620 (Avery et al. 1996; Loesch 1996; Calomiris and Mason 1999; Freddie Mac 2001, 2007; Capone 2002).1Whereas the GSEs actively securitized loans when the nascent subprime market was relatively small, since 2000thisrolehasshiftedentirelytoinvestmentbanksandhedge funds(thenonagencysector).Wearguethatpersistentadherence tothisadhoccutoffbyinvestorswhopurchasesecuritizedpools fromnonagenciesgeneratesadifferentialincreaseintheeaseof securitizationforloans.Thatis,loansmadetoborrowerswhich fall just above the 620 credit cutoff have a higher unconditional likelihoodofbeingsecuritizedandarethereforemoreliquidthan loans below this cutoff.

To evaluate the effect of securitization on screening decisions, weexaminetheperformanceofloansoriginatedbylendersaround this threshold. As an example of our design, consider two borrow- ers,onewithaFICOscoreof621(620+)andtheotherwitha FICO score of 619 (620?), who approach the lender for a loan. Screening to evaluate the quality of the loan applicant involves collecting both hard information, such as the credit score, and soft information, such as a measure of future income stability of theborrower.Hardinformation,bydefinition,issomethingthat iseasytocontractupon(andtransmit),whereasthelenderhas to exert an unobservable effort to collect soft information (Stein 2002).Wearguethatthelenderhasaweakerincentivetobase

- Wediscussthe620ruleofthumbinmoredetailinSectionIIIandinreference to other cutoffs in the lending market in Section IV.G.

origination decisions on both hard and soft information, less care- fully screening the borrower, at 620+, where there is an increasein the relative ease of securitization. In other words, because in- vestors purchase securitized loans based on hard information, the cost of collecting soft information is internalized by lenders when screeningborrowersat620+toalesserextentthanat620?.There- fore,bycomparingtheportfolioofloansoneithersideofthecredit score threshold, we can assess whether differential access to se- curitization led to changes in the behavior of lenders who offered these loans to consumers with nearly identical risk profiles.

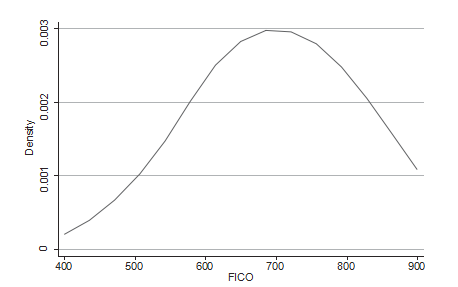

Using a sample of more than one million home purchaseloans during the period 20012006, we empirically confirm that the number of loans securitized varies systematically around the 620 FICO cutoff. For loans with a potential for significant soft informationlow documentationloanswe find that there are morethantwiceasmanyloanssecuritizedabovethecreditthresh- old at 620+than below the threshold at 620?. Because the FICO scoredistributioninthepopulationissmooth(constructedfrom a logistic function; see Figure I), the underlying creditworthiness anddemandformortgageloans(atagivenprice)arethesame for prospective buyers with a credit score of either 620?or 620+. Therefore, these differences in the number of loans confirm that the unconditional probability of securitization is higher above the FICOthreshold;thatis,itiseasiertosecuritize620+loans.

Strikingly, we find that although 620+loans should be of slightly better credit quality than those at 620?, low- documentation loans that are originated above the creditthresholdtendtodefaultwithintwoyearsoforiginationata rate 10%25% higher than the mean default rate of 5% (which amounts to roughly a 0.5%1% increase in delinquencies). As this result is conditional on observable loan and borrower character- istics,theonlyremainingdifferencebetweentheloansaround the threshold is the increased ease of securitization. Therefore,the greater default probability of loans above the credit threshold must be due to a reduction in screening by lenders.

Because our results are conditional on securitization, we con- duct additional analyses to address selection on the part of bor- rowers,lenders,orinvestorsasexplanationsfordifferencesin the performance of loans around the credit threshold. First, we rule out borrower selection on observables, as the loan terms and borrowercharacteristicsaresmoothacrosstheFICOscorethresh- old. Next, selection of loans by investors is mitigated because the

FigureI

FICODistribution(U.S.Population)

The figure presents the FICO distribution in the U.S. population for 2004. Thedata are from an anonymous credit bureau, which assures us that the data exhibitsimilarpatternsduringtheotheryearsofoursample.TheFICOdistributionacross the population is smooth, so the number of prospective borrowers in thelocal vicinity of a given credit score is similar.

decisions of investors (special purpose vehicles, SPVs) are based on the same (smooththrough the threshold) loan and borrower variables as in our data (Kornfeld 2007).

Finally, strategic adverse selection on the part of lenders may also be a concern. However, lenders offer the entire pool of loansto investors, and, conditional on observables, SPVs largely followa randomized selection rule to create bundles of loans out of these pools,suggestingthatsecuritizedloanswouldlooksimilartothose that remain on the balance sheet (Comptrollers Handbook1997; Gorton and Souleles 2006). Furthermore, if at all present, this selection will tend to be more severe below the threshold, thereby biasing the results against our finding any screening effect. Wealso constrain our analysis to a subset of lenders who are not sus- ceptible to strategic securitization of loans. The results for these lenders are qualitatively similar to the findings using the full sample,highlightingthatscreeningisthedrivingforcebehind our results.

Could the 620 threshold be set by lenders as an optimal cut- off for screening that is unrelated to differential securitization?Weinvestigatefurtherusinganaturalexperimentinthepas- sage and subsequent repeal of antipredatory laws in New Jersey (2002) and Georgia (2003) that varied the ease of securitization around the threshold. If lenders used 620 as an optimal cutoff for screening unrelated to securitization, we would expect the pas- sage of these laws to have no effect on the differential screening standards around the threshold. However, if these laws affected the differential ease of securitization around the threshold, our hypothesis would predict an impact on the screening standards. Our results confirm that the discontinuity in the number of loans around the threshold diminished during a period of strict enforce- ment of antipredatory lending laws. In addition, there was a rapid return of a discontinuity after the law was revoked. Importantly, our performance results follow the same pattern, that is, screen- ingdifferentials attenuated onlyduring theperiod of enforcement. Taken together, this evidence suggests that our results are indeed related to differential securitization at the credit threshold and that lenders did not follow the rule of thumb in all instances. Importantly, the natural experiment also suggests that prime- influenced selection is not at play.

Once we have confirmed that lenders are screening more rig- orously at 620?than 620+, we assess whether borrowers were aware of the differential screening around the threshold. Although there is no difference in contract terms around the cutoff, bor- rowersmayhaveanincentivetomanipulatetheircreditscores in order to take advantage of differential screening around the threshold (consistent with our central claim). Aside from out-right fraud, it is difficult to strategically manipulate ones FICO score in a targeted manner and any actions to improve ones score take relatively long periods of time, on the order of three to six months(FairIsaac).Nonetheless,weinvestigatefurtherusing the same natural experiment evaluating the performance effects over a relatively short time horizon. The results reveal a rapid return of a discontinuity in loan performance around the 620 threshold, which suggests that rather than manipulation, our re- sults are largely driven by differential screening on the part of lenders.

As a test of the role of soft information in screening incen- tives of lenders, we investigate thefull documentationloan mar- ket.Theseloanshavepotentiallysignificanthardinformation

because complete background information about the borrowers ability to repay is provided. In this market, we identify another credit cutoff, a FICO score of 600, based on the advice of the three credit repositories. We find that twice as many full documenta- tion loans are securitized above the credit threshold at 600+as below the threshold at 600?. Interestingly, however, we find no significant difference in default rates of full documentation loans originated around this credit threshold. This result suggests that despite a difference in ease of securitization across the thresh-old, differences in the returns to screening are attenuated due to the presence of more hard information. Our findings for full docu- mentation loans suggest that the role of soft information is crucial to understanding what worked and what did not in the existing securitized subprime loan market. We discuss this issue in more detail in Section VI.

This paper connects several strands of the literature. Our evidence sheds new light on the subprime housing crisis, as discussed in the contemporaneous work of Doms, Furlong, and Krainer (2007), Gerardi, Shapiro, and Willen (2007), DellAriccia, Igan, and Laeven (2008), Mayer, Piskorski, and Tchistyi (2008), Rajan, Seru, and Vig (2008), Benmelech and Dlugosz (2009), Mian and Sufi (2009), and Demyanyk and Van Hemert (2010).2This paper also speaks to the literature that discusses the benefits (Kashyap and Stein 2000; Loutskina and Strahan 2007), and the costs (Morrison 2005; Parlour and Plantin 2008) of securitization. In a related line of research, Drucker and Mayer (2008) document how underwriters exploit inside information to their advantage in secondary mortgage markets, and Gorton and Pennacchi (1995), Sufi(2006),andDruckerandPuri(2009)investigatehowcontract terms are structured to mitigate some of these agency conflicts.3

The rest of the paper is organized as follows. Section II pro- vides a brief overview of lending in the subprime market and de- scribes the data and sample construction. Section III discusses the frameworkandempiricalmethodologyusedinthepaper,whereas Sections IV and V present the empirical results in the paper. Sec- tion VI concludes.

- For thorough summaries of the subprime mortgage crisis and the researchwhich has sought to explain it, see Mayer and Pence (2008) and Mayer, Pence, andSherlund (2009).

- Our paper also sheds light on the classic liquidity/incentives trade-off thatis at the core of the financial contracting literature (see Coffee [1991], Diamondand Rajan [2003], Aghion, Bolton, and Tirole [2004], and DeMarzo and Urosevic[2006]).

- LendingintheSubprimeMortgageMarket

- Background

Approximately 60% of outstanding U.S. mortgage debt is traded in mortgage-backed securities (MBS), making the U.S. sec- ondary mortgage market the largest fixed-income market in the world (Chomsisengphet and Pennington-Cross 2006). The bulk of this securitized universe ($3.6 trillion outstanding as of January 2006)iscomposedofagencypass-throughpoolsthoseissuedby Freddie Mac, Fannie Mae, and Ginnie Mae. The remainder, ap- proximately, $2.1 trillion as of January 2006, has been securitized innonagencysecurities.AlthoughthenonagencyMBSmarketisrelativelysmallasapercentageofallU.S.mortgagedebt,it is nevertheless large on an absolute dollar basis. The two mar-ketsareseparatedbasedontheeligibilitycriteriaofloansthat the GSEs have established. Broadly, agency eligibility is estab- lished on the basis of loan size, credit score, and underwriting standards.

Unlike the agency market, the nonagency (referred to as sub- prime in the paper) market was not always this size. This mar-ket gained momentum in the mid- to late 1990s. Inside B&C Lendinga publication that covers subprime mortgage lending extensivelyreports that total subprime lending (B&C origina- tions)grewfrom$65billionin1995to$500billionin2005.Growth in mortgage-backed securities led to an increase in securitization rates (the ratio of the dollar value of loans securitized divided by the dollar value of loans originated) from less than 30% in 1995to over 80% in 2006.

From the borrowers perspective, the primary feature distin- guishing between prime and subprime loans is that the up-front and continuing costs are higher for subprime loans.4The sub- prime mortgage market actively prices loans based on the risk associated with the borrower. Specifically, the interest rate on the loan depends on credit scores, debt-to-income ratios, and the doc- umentation level of the borrower. In addition, the exact pricing may depend on loan-to-value ratios (the amount of equity of the borrower),thelengthoftheloan,theflexibilityoftheinterest rate (adjustable, fixed, or hybrid), the lien position, the property

- Up-frontcostsincludeapplicationfees,appraisalfees,andotherfeesassoci-ated with originating a mortgage. Thecontinuing costs include mortgageinsurancepayments, principal and interest payments, late fees for delinquent payments, andfees levied by a locality (such as property taxes and special assessments).

type, and whether stipulations are made for any prepayment penalties.5

For investors who hold the eventual mortgage-backed secu- rity, credit risk in the agency sector is mitigated by an implicit or explicit government guarantee, but subprime securities have no such guarantee. Instead, credit enhancement for nonagency deals isinmostcasesprovidedinternallybymeansofadealstruc- ture that bundles loans into tranches, or segments of the overall portfolio (Lucas, Goodman, and Fabozzi 2006).

- Data

Our primary data set contains individual loan data leasedfrom LoanPerformance. The database is the only source that pro- vides a detailed perspective on the nonagency securities market. The data include information on issuers, broker dealers/deal un- derwriters, servicers, master servicers, bond and trust adminis- trators, trustees, and other third parties. As of December 2006, more than eight thousand home equity and nonprime loan pools (overseventhousandactive)thatinclude16.5millionloans(more than seven million active) with over $1.6 trillion in outstanding balances were included. LoanPerformance estimates that as of 2006, the data cover over 90% of the subprime loans that are securitized.6The data set includes all standard loan application variables such as the loan amount, term, LTV ratio, credit score, and interest rate typealldata elements that are disclosed and form the basis of contracts in nonagency securitized mortgage pools. We now describe some of these variables in more detail.

For our purpose, the most important piece of information about a particular loan is the creditworthiness of the borrower. The borrowers credit quality is captured by a summary measure calledtheFICOscore.FICOscoresarecalculatedusingvari- ous measures of credit history, such as types of credit in use and

- For example, the rate and underwriting matrix of Countrywide Home Loans, a leading lender of prime and subprime loans, shows how the credit score ofthe borrower and the loan-to-value ratio are used to determine the rates at whichdifferent documentation-level loans are made(www.countrywide.com).

- Note that only loans that are securitized are reported in the LoanPerfor-mance database. Communication with the database provider suggests that theroughly 10% of loans that are not reported are for privacy concerns from lenders.Importantlyforourpurpose,theexclusionisnotbasedonanyselectioncrite-ria that the vendor follows (e.g., loan characteristics or borrower characteristics).Moreover, based on estimates provided by LoanPerformance, the total number ofnonagency loans securitized relative to all loans originated has increased fromabout 65% in early 2000 to over 92% since 2004.

amount of outstanding debt, but donotinclude any information about a borrowers income or assets (Fishelson-Holstein 2005). The software used to generate the score from individual credit re- ports is licensed by the Fair Isaac Corporation to the three major credit repositoriesTransUnion, Experian, and Equifax. These repositories, in turn, sell FICO scores and credit reports to lenders and consumers. FICO scores provide a ranking of potential bor- rowersbytheprobabilityofhavingsomenegativecreditevent in the nexttwo years. Probabilities are rescaled into a range of 400900, though nearly all scores are between 500 and 800, witha higher score implying a lower probability of a negative event.The negative creditevents foreshadowedby the FICO score canbe as small as one missed payment or as large as bankruptcy. Bor- rowers with lower scores are proportionally more likely to haveall types of negative credit events than are borrowers with higher scores.

FICOscoreshavebeenfoundtobeaccurateevenfor low-incomeandminoritypopulations(seeFairIsaacwebsitewww.myfico.com;also see Chomsisengphet and Pennington-Cross [2006]). More importantly, the applicability of scores available at loan origination extends reliably up to two years. By design, FICO measurestheprobabilityofanegativecrediteventoveratwo- year horizon. Mortgage lenders, on the other hand, are interested increditriskoveramuchlongerperiodoftime.Thecontinued acceptanceofFICOscoresinautomatedunderwritingsystems indicates that there is a level of comfort with their value in deter- mining lifetime default probability differences.7Keeping this as a backdrop, most of our tests of borrower default will examine the default rates up to 24 months from the time the loan is originated. Borrower quality can also be gauged by the level of documen- tationcollectedbythelenderwhentakingtheloan.Thedocu- ments collected provide historical and current information about theincomeandassetsoftheborrower. Documentationinthemar- ket (and reported in the database) is categorized as full, limited,or no documentation. Borrowers with full documentation provide verificationofincomeaswellasassets.Borrowerswithlimited documentationprovidenoinformationabouttheirincomebutdo

- An econometric study by Freddie Mac researchers showed that the pre-dictive power of FICO scores drops by about 25% once one moves to a three tofiveyear performance window (Holloway, MacDonald, and Straka 1993). FICOscores are still predictive, but do not contribute as much to the default rate prob-ability equation after the first two years.

provide some information about their assets. No-documentation borrowers provide no information about income or assets, which is a very rare degree of screening lenience on the part of lenders.In our analysis, we combine limited and no-documentation bor- rowers and call them low-documentation borrowers. Our results are unchanged if we remove the very small portion of loans that are no-documentation.

Finally, there is also information about the property being fi- nanced by the borrower, and the purpose of the loan. Specifically, we have information on the type of mortgage loan (fixed rate, ad- justable rate, balloon, or hybrid) and the loan-to-value (LTV) ratio oftheloan,whichmeasurestheamountoftheloanexpressedas a percentage of the value of the home. Typically loans are clas- sified as either for purchase or refinance, though for convenience we focus exclusively on loans for home purchases.8Information about the geography where the dwelling is located (ZIP code) is also available in the database.9

Most of the loans in our sample are for owner-occupiedsingle-family residences, townhouses, or condominiums (single- unit loans account for more than 90% of the loans in our sam-ple). Therefore, to ensure reasonable comparisons, we restrict the loans in our sample to these groups. We also drop nonconven- tional properties, such as those that are FHA- or VA-insured or pledged properties, and also exclude buy down mortgages. Wealso exclude Alt-A loans, because the coverage for these loans in the database is limited. Only those loans with valid FICO scoresare used in our sample. We conduct our analysis for the period January 2001 to December 2006, because the securitization mar- ket in the subprime market grew to a meaningful size post-2000 (Gramlich 2007).

- FrameworkandMethodology

Whenaborrowerapproachesalenderforamortgageloan,the lender asks the borrower to fill out a credit application. In addi- tion,thelenderobtainstheborrowerscreditreportfromthethree credit bureaus. Part of the background information on the appli- cationandreportcouldbeconsideredhardinformation(e.g.,

- Wefindsimilarrulesofthumbanddefaultoutcomesintherefinance

- SeeKeyset(2009)foradiscussionoftheinteractionofsecuritizationandvariationinregulation,drivenbythegeographyofloansandthetypeoflender.

theFICOscoreoftheborrower),whereastherestissoft(e.g., a measure of future income stability of the borrower, how many years of documentation were provided by the borrower, joint in- come status) in the sense that it is less easy to summarize on a legal contract. The lender expends effort to process the soft and hard information about the borrower and, based on this assess- ment, offers a menu of contracts to the borrower. Subsequently, theborrowerdecidestoacceptordeclinetheloancontractoffered by the lender.

Once a loan contract has been accepted, the loan can be soldas part of a securitized pool to investors. Notably, only the hard information about the borrower (FICO score) and the contractual terms (e.g., LTV ratio, interest rate) are used by investors when buying these loans as part of a securitized pool.10In fact, the variables about the borrowers and the loan terms in the LoanPer- formance database are identical to those used by investors and rating agencies to rate tranches of the securitized pool. Therefore, although lenders are compensated for the hard information about theborrower,theincentiveforlenderstoprocesssoftinformation critically depends on whether they have to bear the risk of loans they originate (Gorton and Pennacchi 1995; Parlour and Plantin 2008;Rajan,Seru,andVig2008).Thecentralclaiminthispa- per is that lenders are less likely to expend effort to process soft information as the ease of securitization increases.

WeexploitaspecificruleofthumbattheFICOscoreof 620 that makes securitization of loans more likely if a certainFICO score threshold is attained. Historically, this score was es- tablished as a minimum threshold in the mid-1990s by FannieMae and Freddie Mac in their guidelines on loan eligibility (Avery et al. 1996; Capone 2002). Guidelines by Freddie Mac suggest that FICO scores below 620 are placed in theCautious Review Cate- gory, and Freddie Mac considers a score below 620 as a strong indication that the borrowers credit reputation is not acceptable (Freddie Mac 2001, 2007).11This is also reflected in Fair Isaacs statement, . . .those agencies [Fannie Mae and Freddie Mac], whichbuymortgagesfrombanksandresellthemtoinvestors,

- See Testimony of Warren Kornfeld, Managing Director of Moodys In-vestors Service, before the subcommittee on Financial Institutions and ConsumerCredit, U.S. House of Representatives, May 8, 2007.

- Theseguidelinesappearedatleastasfarbackas1995inaletterbytheExecutiveVicePresidentofFreddieMac(MichaelStamper)totheCEOsand credit officers of all Freddie Mac sellers and servicers (see Online AppendixExhibit 1).

have indicated to lenders that any consumer with a FICO score above620isgood,whileconsumersbelow620shouldresultinfur- therinquiryfromthelenderAlthoughtheGSEsactivelyse-

curitized loans when the nascent subprime market was relatively small, this role shifted entirely to investment banks and hedge funds (the nonagency sector) in recent times (Gramlich 2007).

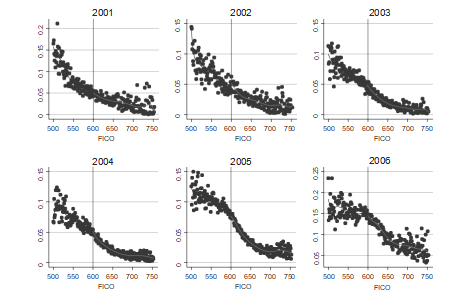

We argue that adherence to this cutoff by subprime MBS in- vestors, following the advice of GSEs, generates an increase in demand for securitized loans that are just above the credit cutoff relative to loans below this cutoff. There is widespread evidence that is consistent with 620 being a rule of thumb in the secu- ritized subprime lending market. For instance, rating agencies (Fitch and Standard and Poors) used this cutoff to determine default probabilities of loans when rating mortgage-backed se- curities with subprime collateral (Loesch 1996; Temkin, Johnson, and Levy 2002). Similarly, Calomiris and Mason (1999) survey the high-risk mortgage loan market and find 620 as a rule of thumbfor subprime loans. We also confirmed this view by conducting a survey of origination matrices used by several of the top fifty orig- inators in the subprime market (a list obtained fromInside B&C Lending; these lenders amount to about 70% of loan volume). The credit threshold of 620 was used by nearly all the lenders.

Because investors purchase securitized loans based on hard information, our assertion is that the cost of collecting soft in- formationisinternalizedbylenderswhenscreeningborrowers at 620?to a greater extent than at 620+. There is widespread anecdotal evidence that lenders in the subprime market review both soft and hard information more carefully for borrowers with credit scores below 620. For instance, the website of Advantage Mortgage,asubprimesecuritizedloanoriginator,claimsthat allloanswithcreditscoresbelow620requireasecondlevel

reviewTherearenoexceptions,regardlessofthestrengthsof

the collateral or capacity components of the loan.12By focusingon the lender as a unit of observation, we attempt to learn about the differential impact ease of securitization had on the behaviorof lenders around the cutoff.

To begin with, our tests empirically identify a statistical dis- continuity in the distribution of loans securitized around thecreditthresholdof620.Inordertodoso,weshowthatthenumber

- Thispositionforloansbelow620isreflectedinlendingguidelinesofnumerous other subprime lenders.

of loans securitized dramatically increases when we move along the FICO distribution from 620?to 620+. We argue that this is equivalent to showing that the unconditional probability of se- curitizationincreasesasonemovesfrom620?to620+.Tosee

this,denoteN620+andN620?asthenumbersofloanssecuritized

ss

at620+and620?,respectively.ShowingthatN620+>N620?is

ss

equivalenttoshowingthatN620+/Np>N620?/Np,whereNpis

ss

the number of prospective borrowers at 620+or 620?. If we as- sume that the numbers of prospective borrowers at 620+and 620?aresimilar,thatis,N620??N620+=Np(areasonableassumption,

pp

as discussed below), then the unconditional probability of securi- tization is higher at 620+. We refer to the difference in these unconditional probabilities as the differentialease of securitiza- tionaround the threshold. Notably, our assertion of differential screeningbylendersdoesnotrelyonknowledgeoftheproportion ofprospectiveborrowersthatapplied,wererejected,orwereheld on the lenders balance sheet. We simply require that lenders are aware that a prospective borrower at 620+has a higher likelihood of eventual securitization.

Wemeasuretheextentofthejumpbyusingtechniquesthat are commonly used in the literature on regression discontinu- ity (e.g., see DiNardo and Lee [2004]; Card, Mas, and Rothstein [2008]). Specifically, we collapse the data on each FICO score (500 800)iand estimate equations of the form

(1)Yi=?+?Ti+?f(FICO(i))+?Tif(FICO(i))+i,

whereYiis the number of loans at FICO scorei,Tiis an in- dicatorthattakesavalueof1atFICO? 620andavalueof0 ifFICO<620andiisamean-zeroerrorterm.f(FICO)andTf(FICO)areflexibleseventh-orderpolynomials,withthegoal of these functions being to fit the smoothed curves on either side of the cutoff as closely to the data presented in the figures aspossible.13f(FICO)isestimatedfrom620?totheleft,andTf(FICO) is estimated from 620+to the right. The magnitude of the discontinuity,?, is estimated by the difference in these two smoothed functions evaluated at the cutoff. The data arere-centeredsuch that FICO=620 corresponds to 0, thus at the

- WehavealsoestimatedthesefunctionsoftheFICOscoreusingthird-orderand fifth-order polynomials in FICO, as well as relaxing parametric assumptionsand estimating using local linear regression. The estimates throughout are notsensitivetothespecificationoftheseInSectionIV,wealsoexaminethe size and power of the test using the seventh-order polynomial specificationfollowing the approach of Card, Mas, and Rothstein (2008).

cutoff the polynomials are evaluated at 0 and drop out of the cal- culation,whichallows?tobeinterpretedasthemagnitudeof thediscontinuityattheFICOthreshold.Thiscoefficientshould be interpreted locally in the immediate vicinity of the credit score threshold.

After documenting a large jump at the ad-hoc credit thresh- olds,wefocusontheperformanceoftheloansaroundthesethresh- olds. We evaluate the performance of the loans by examining the default probability of loansthat is, whether or not the loan de- faultedtmonths after it was originated. If lenders screen similarly for the loan of credit quality 620+and the loan of 620?credit qual- ity, there should not be any discernible differences in default rates of these loans. Our maintained claim is that any differences in de- fault rates on either side of the cutoff, after controlling for hard information, should be only due to the impact that securitization has on lenders screening standards.

This claim relies on several identification assumptions. First, asweapproachthecutofffromeitherside,anydifferencesin the characteristics of prospective borrowers are assumed to be random. This implies that the underlying creditworthiness andthedemandformortgageloans(atagivenprice)isthesame for prospective buyers with a credit score of 620?or 620+. This seems reasonable as it amounts to saying that the calculation Fair Isaac performs (using a logistic function) to generate credit scores has a random error component around any specific score. Figure I shows the FICO distribution in the U.S. population in 2004. These data are from an anonymous credit bureau that assures us thatthe data exhibit similar patterns during the other years of our sample.NotethattheFICOdistributionacrossthepopulationissmooth,sothenumberofprospectiveborrowersacrossagiven

creditscoreissimilar(intheexampleabove,N620??N620+=Np).

pp

Second,weassumethatscreeningiscostlyforthelender. The collection of informationhard systematic data (e.g., FICO score) as well as soft information (e.g., joint income status) about thecreditworthinessoftheborrowerrequirestimeandeffortby loan officers. If lenders did not have to expend resources to collect information,itwouldbedifficulttoarguethatthedifferences in performance we estimate are a result of ease of securitization around the credit threshold affecting banks incentives to screen and monitor. Again, this seems to be a reasonable assumption (see Gorton and Pennacchi [1995]).

Note that our discussion thus far has assumed that there is no explicitmanipulationofFICOscoresbythelendersorborrowers.

TABLE ISummaryStatistics

PanelA:Summarystatisticsbyyear

Lowdocumentation Fulldocumentation

|

Numberofloans |

Meanloan-to-value |

MeanFICO |

Numberofloans |

Meanloan-to-value |

MeanFICO |

||

|

2001 |

35,427 |

81.4 |

630 |

101,056 |

85.7 |

604 |

|

|

2002 |

53,275 |

83.9 |

646 |

109,226 |

86.4 |

613 |

|

|

2003 |

124,039 |

85.2 |

657 |

194,827 |

88.1 |

624 |

|

|

2004 |

249,298 |

86.0 |

658 |

361,455 |

87.0 |

626 |

|

|

2005 |

344,308 |

85.5 |

659 |

449,417 |

86.9 |

623 |

|

|

2006 |

270,751 |

86.3 |

655 |

344,069 |

87.5 |

621 |

PanelB:Summarystatisticsofkeyvariables

Lowdocumentation Fulldocumentation

|

Mean |

Std.dev. |

Mean |

Std.dev. |

||

|

Averageloansize($000) |

189.4 |

132.8 |

148.5 |

116.9 |

|

|

FICOscore |

656.0 |

50.0 |

621.5 |

51.9 |

|

|

Loan-to-valueratio |

85.6 |

9.8 |

87.1 |

9.9 |

|

|

Initialinterestrate |

8.3 |

1.8 |

8.2 |

1.9 |

|

|

ARM(%) |

48.5 |

50.0 |

52.7 |

49.9 |

|

|

Prepaymentpenalty(%) |

72.1 |

44.8 |

74.7 |

43.4 |

Notes.InformationonsubprimehomepurchaseloanscomesfromLoanPerformance.Sampleperiodis20012006. See text for sample selection.

However, the borrower may have incentives to do so if loan con- tracts or screening differ around the threshold. Our analysis in Section IV.F focuses on a natural experiment and shows that the effects of securitization on performance are not being driven by strategic manipulation.

- MainEmpiricalResults

- DescriptiveStatistics

As noted earlier, the nonagency market differs from the agency market on three dimensions: FICO scores, loan-to-value ratios, and the amount of documentation asked of the borrower. We next look at the descriptive statistics of our sample, with spe- cial emphasis on these dimensions. Our analysis uses more than one million loans across the period 2001 to 2006. As mentioned earlier, the nonagency securitization market has grown dramat- icallysince2000,whichisapparentinPanelAofTableI,which

shows the number of subprime loans securitized across years. These patterns are similar to those described in Gramlich (2007) andDemyanykandVanHemert(2010).Themarkethaswitnessed an increase in the number of loans with reduced hard information in the form of limited or no documentation. Note that whereas limited documentation provides no information about income but does provide some information about assets, a no-documentation loanprovidesinformationaboutneitherincomenorassets.In our analysis we combine both types of limited-documentation loans and denote them aslow-documentation loans. The full- documentationmarketgrewby445%from2001to2005,whereas the number of low-documentation loans grew by 972%.

We find similar trends for loan-to-value ratios and FICOscoresinthetwodocumentationgroups.LTVratioshavegone up over time, as borrowers have put less and less equity into their homes when financing loans. This increase is consistent with bet- ter willingness of marketparticipantsto absorbrisk. In fact, thisis often considered the bright side of securitizationborrowers are able to borrow at better credit terms because risk is being borne by investors who can bear more risk than individual banks. Panel A also shows that average FICO scores of individuals who access the subprime market have been increasing over time. The mean FICO score among low-documentation borrowers increased from 630 in 2001 to 655 in 2006. This increase in average FICO scores is consistent with the rule of thumb leading to a larger ex- pansion of the market above the 620 threshold. Average LTV ra- tios are lower and FICO scores higher for the low-documentation as compared to the full-documentation sample. This possibly re- flects the additional uncertainty lenders have about the quality of low-documentation borrowers.

Panel B compares the low- and full-documentation segments of the subprime market on a number of the explanatory vari-ables used in the analysis. Low-documentation loans are on av- erage larger and are given to borrowers with higher credit scores than loans where full information on income and assets is pro- vided. However, the two groups of loans have similar contract termssuchasinterestrate,loan-to-value,prepaymentpenal- ties, and whether the interest rate is adjustable or not. Ouranalysisbelowfocusesfirstonthelow-documentationsegment of the market; we explore the full-documentation market in Section V.

- EstablishingtheRuleofThumb

We first present results that show that large differences exist in the number of low-documentation loans that are securitized aroundthecreditthresholdwedescribedearlier.Wethenexamine whether this jump in securitization has any consequences on the subsequent performance of the loans above and below this credit threshold.

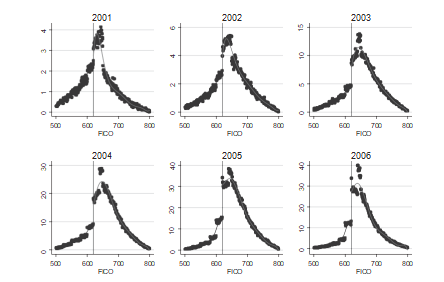

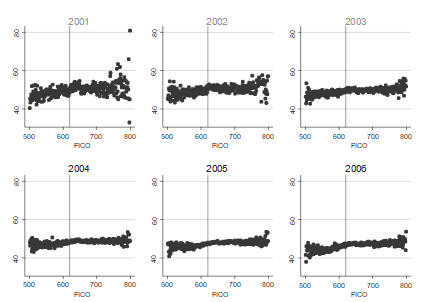

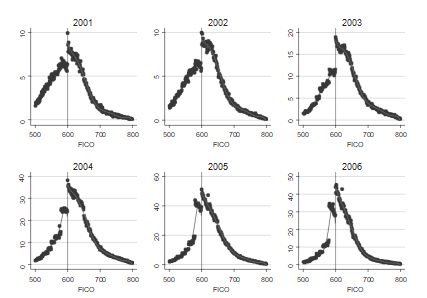

As mentioned in Section III, the rule of thumb in the lending marketimpactstheeaseofsecuritizationaroundacreditscore of 620. We therefore expect to see a substantial increase in the number of loans just above this credit threshold as compared to number of loans just below this threshold. In order to examinethis, we start by plotting the numberof loansat eachFICO scorein the two documentation categories around the credit cutoff of 620 across years starting with 2001 and ending in 2006. As can be seen from Figure II, there is a marked increase in number of low- documentation loans at 620+relative to the number of loans at 620?. We do not find any such jump for full-documentation loansat FICO of 620.14Given this evidence, we focus on the 620 credit threshold for low-documentation loans.

From Figure II, it is clear that the number of loans see roughly a100%jumpin2004forlow-documentationloansacrossthecredit score of 620there are twice as many loans securitized at 620+at 620?. Clearly, this is consistent with the hypothesis that the easeof securitization is higher at 620+than at scores just below this credit cutoff.

Toestimatethejumpsinthenumberofloans,weusethe methodsdescribedaboveinSectionIIIusingthespecification providedinequation(1).AsreportedinTableII,wefindthat low-documentation loans see a dramatic increase above the credit threshold of 620. In particular, the coefficient estimate (?) is sig- nificantatthe1%levelandisonaveragearound110%(from73% to193%)higherfor620+ascomparedto620?forloansduringthe sample period. For instance, in 2001, the estimated discontinuity in Panel A is 85. The mean average number of low-documentation loansataFICOscorefor2001is117.Theratioisaround73%. These jumps are plainly visible from the yearly graphs in Figure I. Inaddition,weconductpermutationtests(orrandomiza-tiontests),wherewevarythelocationofthediscontinuity(Ti)

- Wewillelaboratemoreonfull-documentationloansinSection

FigureII

NumberofLoans(Low-Documentation)

The figure presents the data for number of low-documentation loans (in 00s).WeplottheaveragenumberofloansateachFICOscorebetween500and800.As can be seen from the graphs, there is a large increase in the number of loansaround the 620 credit threshold (i.e., more loans at 620+as compared to 620?)from 2001 onward. Data are for loans originated between 2001 and 2006.

TABLEII

DiscontinuityinNumberofLow-DocumentationLoans

YearFICO ? 620(?)t-stat ObservationsR2Mean

|

2001 |

36.83 |

(2.10) |

299 |

.96 |

117 |

|

2002 |

124.41 |

(6.31) |

299 |

.98 |

177 |

|

2003 |

354.75 |

(8.61) |

299 |

.98 |

413 |

|

2004 |

737.01 |

(7.30) |

299 |

.98 |

831 |

|

2005 |

1,721.64 |

(11.78) |

299 |

.99 |

1,148 |

|

2006 |

1,716.49 |

(6.69) |

299 |

.97 |

903 |

Pooledestimate(t-stat)[permutationtestp-value] 781.87(4.14)[.003]

Notes.Thistablereportsestimatesfromaregressionthatusesthenumberoflow-documentationloansateachFICOscoreasthedependentvariable.Inordertoestimatethediscontinuity(FICO?620)foreachyear,wecollapsethenumberofloansateachFICOscoreandestimateflexibleseventh-orderpolynomialsoneithersideofthe620cutoff,allowingforadiscontinuityat620.Wereportt-statisticsinparentheses.Permutationtests, which allow for a discontinuity at every point in the FICO distribution, confirm that jumps for eachyeararesignificantlylargerthanthosefoundelsewhereinthedistribution(seeSectionIV.Bformoredetails).Forbrevity,wereportapermutationtestestimatefrompooledregressionswithtimefixedeffectsremovedtoaccountforvintageeffects.FICO=620hasthesmallestpermutationtestp-value(andisthusthelargestoutlier) amongallthe visible discontinuities in our sample.

acrosstherangeofallpossibleFICOscoresandreestimateequa- tion (1). The test treats every value of the FICO distribution asa potential discontinuity, and estimates the magnitude of the observed discontinuity at each point, forming a counter factual distribution of discontinuity estimates. This is equivalent to a bootstrapping procedure that varies the cutoff but does not re- sampletheorderofthepointsinthedistribution(Johnstonand DiNardo1996).Wethencomparethevalueoftheestimateddis- continuityat620tothecounterfactualdistributionandconstruct ateststatisticbasedontheasymptoticnormalityofthecounter- factualdistributionandreportthep-valuefromthistest.Thenull hypothesisisthattheestimateddiscontinuityataFICOscoreof 620isthemeanofthe300possiblediscontinuities.15

Theprecisionofthepermutationtestislimitedbythenumber of observations used at each FICO score. As a result, regressions that pool across years provide the greatest power for statistical testing. While constructing the counterfactuals, we therefore use pooledspecificationswithyearfixedeffectsremovedtoaccountfor differences in vintage. The result of this test is shown in Table II andshowsthattheestimateat620forlow-documentationloansis a strong outlier relative to the estimated jumps at other locations in the distribution. The estimated discontinuity when the yearsare pooled together is 780 loans with a permutation testp-valueof .003. In summary, if the underlying creditworthiness and the demand for mortgage loans are the same for potential buyers with a credit score of 620?or 620+, this result confirms that it is easier to securitize loans above the FICO threshold.

- ContractTermsandBorrowerDemographics

Before examining the subsequent performance of loans aroundthecreditthreshold,wefirstassesswhetherthereare any differences in hard informationeither in contract terms orin other borrower characteristicsaround this threshold. The en- dogeneityofcontractualtermsbasedontheriskinessofborrowers may lead to different contracts and hence different types of bor- rowers obtaining loans around the threshold in a systematic way.

- In unreported tests, we also conduct a falsification simulation exercisefollowingCard, Mas,andRothstein(2008). Inparticular, we applyourspecificationtodatageneratedbyacontinuousWerejectthenullhypothesisofnoeffect(using a two-sided 5% test) in 6.0% of the simulations, indicating that the size ofour test is reasonable. A similar test with data generated by a discontinuousprocesssuggeststhatthepowerofourtestisalsoreasonable.Werejectthenullof no effect about 92% of the times (in a two-sided 5% test) in this case.

FigureIII

InterestRates(Low-Documentation)

The figure presents the data for interest rate (in %) on low-documentationloans. We plot average interest rates on loans at each FICO score between 500 and800. As can be seen from the graphs, there is no change in interest rates aroundthe 620 credit threshold (i.e., more loans at 620+as compared to 620?) from 2001onward. Data are for loans originated between 2001 and 2006.

Though we control for the possible contract differences when we evaluate the performance of loans, it is a source of insight to ex- amine whether borrower and contract terms also systematically differ around the credit threshold.

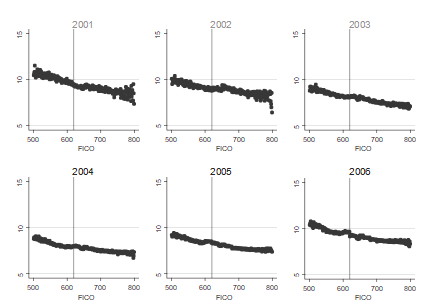

We start by examining the contract termsLTV ratio and in- terest ratesacross the credit threshold. Figures III and IV show the distributions of interest rates and LTV ratios offered on low- documentation loans across the FICO spectrum. As is apparent,wefindtheseloantermstobeverysimilarthatis,wefindnodif- ferencesincontracttermsforlow-documentationloansaboveand belowthe620creditscore.Wetestthisformallyusinganapproach equivalenttoequation(1),replacingthedependentvariableYiin the regression framework with contract terms (loan-to-value ratiosandinterestrates)andpresenttheresultsinAppendix

I.A. Our results suggest that there is no difference in loan terms across the credit threshold. For instance, for low-documentation loansoriginatedin2006,theaverageloan-to-valueratioacrossthe

FigureIV

Loan-to-ValueRatio(Low-Documentation)

Thefigurepresentsthedataforloan-to-valueratio(in%)onlow-documentationloans. We plot average loan-to-value ratios on loans at each FICO score between500 and 800. As can be seen from the graphs, there is no change in loan-to-valuearound the 620 credit threshold (i.e., more loans at 620+as compared to 620?)from 2001 onward. Data are for loans originated between 2001 and 2006.

collapsed FICO spectrum is 85%, whereas our estimated disconti- nuity is only ?1.05%, a 1.2% difference. Similarly for the interest rate, for low-documentation loans originated in 2005, the average interest rate is 8.2%, and the difference on either side of the credit score cutoff is only about ?0.091%, a 1% difference. Permutation tests reported in Appendix I.D confirm that these differences are not outliers relative to the estimated jumps at other locations in the distribution.

Additional contract terms, such as the presence of a pre- paymentpenalty,orwhethertheloanisARM,FRM,orinter- est only/balloon are also similar across the 620 threshold (results not shown). In addition, if loans have second liens, then a com- bined LTV (CLTV) ratio is calculated. We find no difference in the CLTV ratios around the threshold for those borrowers with more than one lien on the home. Finally, low-documentation loans of- tendonotrequire thatborrowers provide informationabout their

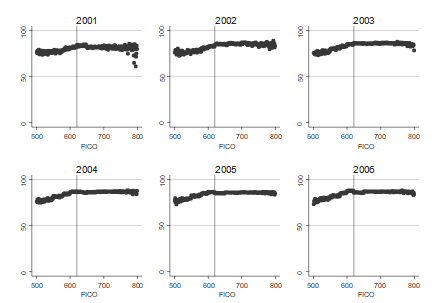

FigureV

MedianHouseholdIncome(Low-Documentation)

The figure presents median household income (in 000s) of ZIP codes in whichloansaremadeateachFICOscorebetween500and800.Ascanbeseenfromthe graphs, there is no change in median household income around the 620 creditthreshold (i.e., more loans at 620+as compared to 620?) from 2001 onward. Weplotted similar distributions for average percent minorities taking loans and av-erage house size and found no differences around the credit thresholds. Data arefor loans originated between 2001 and 2006.

income, so only a subset of our sample provides a debt-to-income (DTI) ratio for the borrowers. Among this subsample, there is no difference in DTI across the 620 threshold in low-documentation loans. For brevity, we report only the permutation tests for these contract terms in Appendix I.D.

Next, we examine whether the characteristics of borrowers differ systematically across the credit threshold. In order to eval- uatethis,welookatthedistributionofthepopulationofborrowers across the FICO spectrum for low-documentation loans. The data on borrower demographics come from Census 2000 and are at the ZIP code level. As can be seen from Figure V, median household incomesoftheZIPcodesofborrowersaroundthecreditthresholds look very similar for low-documentation loans. We plotted similar distributions for average percent minorities residing in the ZIP codeandaveragehousevalueintheZIPcodeacrosstheFICO

spectrum (unreported) and again find no differences across the credit threshold.16

We use the same specification as equation (1), this time with the borrower demographic characteristics as dependent variables and present the results formally in Appendix I.B. Consistent with the patterns in the figures, permutation tests (unreported) reveal no differences in borrower demographic characteristics around the credit score threshold. Overall, our results indicate that ob- servable characteristics of loans and borrowers are not different around the credit threshold.

- PerformanceofLoans

We now focus on the performance of loans that are originated close to the credit score threshold. Note that our analysis in Sec- tionIV.Csuggeststhatthereisnodifferenceintermsofobservable hard information about contract terms or about borrower demo- graphic characteristics across the credit score thresholds. Never- theless, we will control for these differences when evaluating the subsequent performance of loans in our logit regressions. If there is any remaining difference in the performance of the loans above and below the credit threshold, it can be attributed to differences in unobservable soft information about the loans.

We estimate the differences in default rates on either side of the cutoff using the same framework as equation (1), using the dollar-weighted fraction of loans defaulted within ten to fifteen months of origination as the dependent variable,Yi. This fractionis calculated as the dollar amount of unpaid loans in default di- videdbythetotaldollaramountoriginatedinthesamecohort.We classify a loan as under default if any of the conditions is true: (a) payments on the loan are 60+days late as defined by the Office of Thrift Supervision; (b) the loan is in foreclosure; or (c) the loan is real estate owned (REO), that is, the bank has retaken possession of the home.17

- Of course, because the census data are at the ZIP code level, we are tosome extent smoothing our distributions. We note, however, that when we conductour analysis on differences in number of loans (from Section IV.B), aggregatedat the ZIP code level, we still find jumps across the credit threshold within eachindividual ZIP code.

- Although two different definitions of delinquency are used in the industry(Mortgage Bankers Association (MBA) definition and Office of Thrift Supervision(OTS) definition), we have followed the more stringent OTS definition. WhereasMBA starts counting days a loan has been delinquent from the time a payment ismissed, OTS counts days a loan is delinquent one monthafterthe first payment is

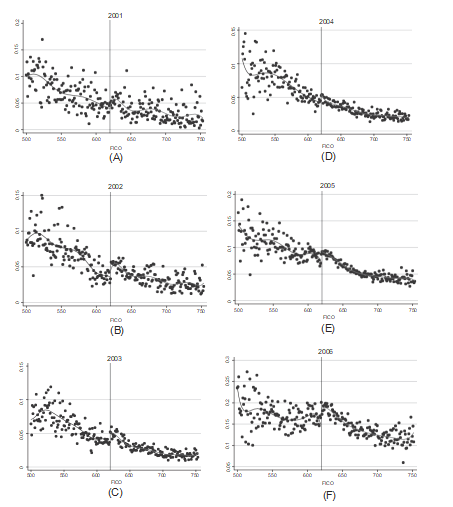

We collapse the data into one-point FICO bins and estimate seventh-order polynomials on either sideof the threshold for each year.Byestimatingthemagnitudeof?ineachyearseparately, we ensure that no one cohort (or vintage) of loans is driving our results. As shown in Figures VI.A to VI.F, the low-documentation loans exhibit discontinuities in default rates at the FICO score of 620. A year-by-year estimate is presented in Panel A of Table III. Contrary to what one might expect, around the credit threshold, we find that loans with higher credit scores actually defaultmore oftenthanlowercreditloansinthepost-2000period.Inparticular, forloansoriginatedin2005,theestimateof?is0.023(t-stat

= 2.10), and the mean delinquency rate is 0.078, suggesting a 29% increase in defaults to the right of the credit score cutoff. Similarly,in2006,theestimatedsizeofthejumpis0.044(t-stat

=2.68),andthemeandelinquencyrateforallFICObinsis0.155, whichisagaina29%increaseindefaultsaroundtheFICOscore threshold.

Panel B presents results of permutation tests, estimated onthe residuals obtained after pooling delinquency rates acrossyears and removing year effects. Besides the 60+late delinquency definitionusedinPanelA,wealsoclassifyaloanasindefaultif it is 90+late in payments and if it is in foreclosure or REO. Our approach yields similar, if not stronger, results. Compared to 620?loans, 620+loans are on average 2.8% more likely to be in arrears of 90+days and 2.5% more likely to be in foreclosure or REO. Permutationtestp-valuesconfirmthatthejumpindefaultsat 620 using all the definitions of default are extreme outliers to the rest of the delinquency distribution. For instance, with default de- fined as foreclosure/REO, thep-value for the discontinuity at 620 is .004. That we find similar results using different default defini- tions is consistent with high levels of rollover, whereby loans that are delinquent continue to reach deeper levels of delinquency. As shown in Online Appendix Table 1, more than 80% of loans that are 60 days delinquent reach 90+days delinquent within a year, and 66% of loans that are 90 days delinquent reach foreclosure twelve months after in the low documentation market.

Although previous default definitions were dollar-weighted, we also use the raw number of loans in default to estimate the magnitude of the discontinuity in loan performance around the FICOthreshold.Theunweightedresultswith60+delinquency arealsopresentedinPanelB,andcontinuetoexhibitapattern ofhighercreditscoresleadingtohigherdefaultratesacrossthe

FigureVI

Annual Delinquencies for Low-Documentation Loans Originated in 20012006Thefigurespresentthepercentageoflow-documentationloansoriginatedin

2001(A),2002(B),2003(C),2004(D),2005(E),and2006(F)thatbecamedelinquent.We plot the dollar-weighted fractions of the pools that become delinquent for one-point FICO bins between scores of 500 and 750. The vertical lines denote the 620cutoff, and a seventh-order polynomial is fitted to the data on either side of thethreshold. Delinquencies are reported between ten and fifteen months for loansoriginated in the year.

TABLE III

DelinquenciesinLow-DocumentationLoansaroundtheCreditThreshold

Panel A: Dollar-weighted fraction of loans defaulted (60+ delinquent)Year FICO ? 620 (?)t-stat ObservationsR2Mean

|

2001 |

0.005 |

(0.44) |

254 |

.58 |

0.053 |

|

2002 |

0.010 |

(2.24) |

254 |

.75 |

0.051 |

|

2003 |

0.022 |

(3.47) |

254 |

.83 |

0.043 |

|

2004 |

0.013 |

(1.86) |

254 |

.79 |

0.049 |

|

2005 |

0.023 |

(2.10) |

254 |

.81 |

0.078 |

|

2006 |

0.044 |

(2.68) |

253 |

.57 |

0.155 |

Panel B: Permutation tests for alternative default definitions(pooled 20012006 with time fixed effects)

Permutation

PanelC:Delinquencystatusofloans

Pr(delinquency)=1

|

(1) |

(2) |

(3) |

(4) |

|

|

FICO?620 |

0.12 |

0.48 |

0.12 |

0.48 |

|

[0.004] |

[0.011] |

[0.004] |

[0.011] |

|

|

(3.42) |

(2.46) |

(2.10) |

(2.48) |

|

|

Observations |

1,393,655 |

1,393,655 |

1,393,655 |

1,393,655 |

|

PseudoR2 |

.088 |

.116 |

.088 |

.116 |

|

Othercontrols |

Yes |

Yes |

Yes |

Yes |

|

FICO?620?othercontrols |

No |

Yes |

No |

Yes |

|

Timefixedeffects |

No |

Yes |

No |

Yes |

|

Clusteringunit |

LoanID |

LoanID |

Vintage |

Vintage |

|

Meandelinquency(%) |

4.45 |

Notes.InPanelA,weestimatethedifferencesindefaultratesusingaflexibleseventh-orderpolynomialon either side of the 620 cutoff, allowing for a discontinuity at 620. The 60+dollar-weighted fraction of loansdefaulted within 1015 months is the dependent variable. In Panel B, we present estimates from permutationtests from pooled regressions with time fixed effects removed to account for vintage effects using specificationsimilar to PanelA. Permutationtestsconfirm thatthe discontinuityat 620has the smallestp-value (andisthuslargestoutlier)inoursample.Weusealternativedefinitionsofdefaultsasthedependentvariable.In

Panel C, we estimate differences in default rates on either side of the 620 FICO cut off using a logit regression.Thedependentvariableisthedelinquencystatusofaloaninagivenmonththattakesavalue1iftheloanis classified as under default, as defined in the text. Controls include borrower and loan terms discussed inSection IV.t-statistics are reported in parentheses (marginal effects are reported in square brackets).

FigureVII

DelinquenciesforLow-DocumentationLoans(20012006)

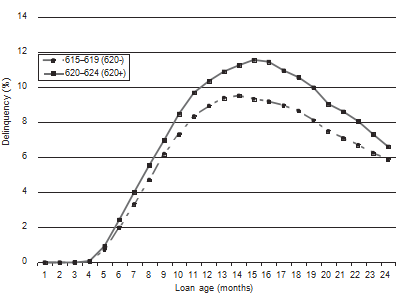

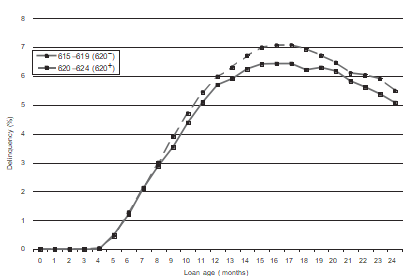

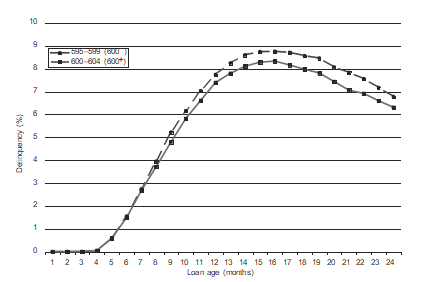

The figure presents the percent of low-documentation loans (dollar-weighted)originatedbetween2001and2006thatsubsequentlybecamedelinquent.Wetrackloans in two FICO buckets615619 (620?) dashed and 620624 (620+) solidfromtheiroriginationdateandplottheaverageloansthatbecomedelinquenteachmonth after the origination date. As can be seen, the higher credit score bucketdefaultsmorethan the lower credit score bucket for the post-2000 period. Forbrevity, we do not report plots separately for each year of origination. The effectsshown here in the pooled 20012006 plot are apparent in every year.

620 threshold. In fact, the results are statistically stronger thanthe 60+weighted results, with a permutation testp-value basedon the pooled estimates of .004 and the discontinuity estimate being significant in all the years (unreported; see Online Appendix Figure 4).

To show how delinquency rates evolve over the age of the loan,inFigureVIIweplotthedelinquencyratesof620+and 620?for low-documentation loans (dollar-weighted) by loan age. As discussed earlier, we restrict our analysis to about two years after the loan has been originated. As can be seen from the figure, the differences in the delinquency rates are stark. The differences begin around four months after the loans have been originatedand persist up to two years. Differences in default rates also seem quitelargeintermsofmagnitudes.Thosewithacreditscoreof 620?are about 20% less likely to default after a year as compared to loans with credit score 620+.18

Analternativemethodologyistomeasuretheperformance of each unweighted loan by tracking whether or not it became delinquent and estimate logit regressions of the following form:

- Yikt=??+?Tit+?1Xikt+?1Tit?Xikt+?t+ikt.

Thislogisticapproach complements the regression discontinuity framework, as we restrict the sample to the ten FICO points in theimmediatevicinityof620inordertomaintainthesamelocal interpretation of the RD results. Moreover, we are also able to directly control for the possibly endogenous loan terms around the threshold. The dependent variable is an indicator variable (Delinquency) for loanioriginated in yeartthat takes a valueof 1 if the loan is classified as under default in monthkafter origination as defined above. We drop the loan from the regression once it is paid out after reaching the REO state.Ttakes the value 1 if FICO is between 620 and 624, and 0 if it is between 615 and 619 for low-documentation loans, thus restricting the analysistotheimmediatevicinityofthecutoffs.Controlsinclude FICO scores, the interest rate on the loan, loan-to-value ratio, and borrower demographic variables, as well as interaction of these variables withT. We also include a dummy variable for the type of loan (adjustable or fixed rate mortgage). We control forthepossiblenonlineareffectofageoftheloanondefaultsby includingthreedummyvariableswhichtakeavalueof1ifthe month since origination is 010, 1120, and more than 20 months, respectively.Yearoforiginationfixedeffectsareincludedinthe estimationandstandarderrorsareclusteredattheloanlevelto account for multiple loan delinquency observations in the data.

AscanbeseenfromthelogitcoefficientsinPanelCofTa- ble III, results from this regression are qualitatively similar to those reported in the figures. In particular, we find that?is pos- itive when we estimate the regressions for low-documentation loans.Theeconomicmagnitudesaresimilartothoseinthe

- Note that Figure VII does not plot cumulative delinquencies. As loansare paid out, say after a foreclosure, the unpaid balance for these loans fallsrelative to the time when they entered into a 60+This explains the dip indelinquencies in the figure after about twenty months. Our results are similar ifweplotcumulativedelinquencies,ordelinquenciesthatarecalculatedusingtheunweightednumberofloans.Alsonotethatthefactthatwefindnodelinquenciesearly on in the duration of the loan is not surprising, given that originators arerequiredtotakebackloansontheirbooksiftheloansdefaultwithinthreemonths.

figures as well. For instance, keeping all other variables at their mean levels, low-documentation loans with credit score 620?are about 10%25% less likely to default after a year than low- documentation loans with credit score 620+. These are large magnitudesfor instance, note that the mean delinquency ratefor low-documentation loans is around 4.45%; the economic mag- nitudeoftheeffectsincolumn(2)suggeststhatthedifference in the absolute delinquency rate between loans around the credit threshold is around 0.5%1% for low documentation loans.19

To account for the possibility that lax screening might be cor- related across different loans within the same vintage, we cluster the loans for each vintage and report the results in columns (3) and (4). Note that the RD regressions (Panel A) estimated sep- arately by year also alleviate concerns about correlated errors across different loans with the same vintage.

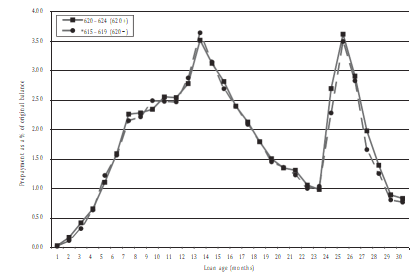

In the mortgage market, the other way for loans to leave the poolistoberepaidinfullthroughrefinancingoroutrightpur- chase, known as prepayment. This prepayment risk decreases the returntoinvestinginmortgage-backedsecuritiesinamanner similartodefaultrisk(see,e.g.,Gerardi,Shapiro,andWillen[2007]andMayer,Piskorski,andTchistyi[2008]).Toassesswhether there are any differences in actual prepayments around the 620 threshold, we plot the prepayment seasoning curve for all years 20012006 in Figure VIII. As can be observed, prepayments of 620+and 620?borrowers in the low-documentation market are similar (also see permutation test in Appendix I.D). Nevertheless, to formally account for prepayment rates, we also estimate a com- petingriskmodelusingbothprepaymentanddefaultasmeans for exiting the sample. We use the Cox proportional hazard model basedontheeconometricspecificationfollowingDeng,Quigley, and Van Order (2000). In unreported tests (Online Appendix Ta- ble 6), we find results that are similar to our logistic specification. Finally, the reported specification uses five-point bins of FICO scores around the threshold, but the results are similar (thoughless precise) if we restrict the bins to fewer FICO scores on either side of 620 (Online Appendix Table 2). This issue is also fully ad- dressed by the regression discontinuity results reported in Panels AandB,whichuseindividualFICOscorebinsastheunitsof

- Our logistic specification is equivalent to a hazard model if we drop loansas soon as they hit the first indicator of delinquency (sixty days in default) andinclude a full set of duration dummies. Doing so does not change the nature of our

FigureVIII

ActualPrepaymentsforLow-DocumentationLoans(20012006)

The figure presents the percentage of low-documentation loans (dollarweighted)originatedbetween2001and2006thatsubsequentlywereprepaid.We track loans in two FICO buckets615619 (620?) dashed and 620624 (620+)solidfrom their origination dates and plot the average loans that prepaid eachmonth after the origination date. As can be seen, there are no differences in pre-payments between the higher and lower credit score buckets. For brevity, we donot report plots separately for each year of origination. The effects shown here inthe pooled 20012006 plot are apparent in every year.

observation. In sum, we find that even after controlling for all ob- servable characteristics of the loan contracts or borrowers, loans madetoborrowerswithhigherFICOscoresperformworsearound the credit threshold.

IV.E.SelectionConcerns

Because our results are conditional on securitization, we con- ductadditionalanalysestoaddressselectionexplanationsonac- countofborrowers,investors,andlendersforthedifferencesin theperformanceofloansaroundthecreditthreshold.First,con- tract terms offered to borrowers above the credit threshold might differ from those below the threshold and attract a riskier pool of borrowers. If this were the case, it would not be surprising if theloansabovethecreditthresholdperformedworsethanthose belowit.AsshowninSectionIV.C,loantermsaresmooththrough the FICO score threshold. We also investigate the loan terms in

more detail than in Section IV.C by examining the distribution of interest rates and loan-to-value ratios of contracts offered around 620 for low-documentation loans.

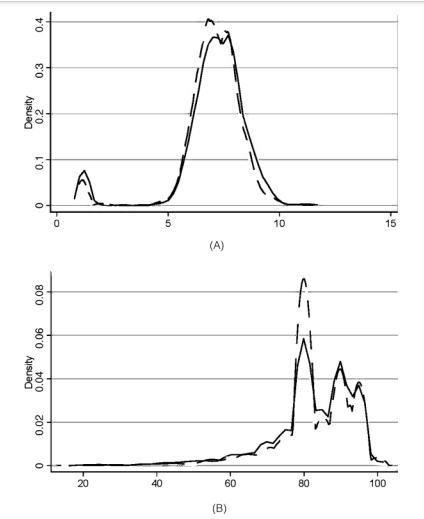

Figure IX.A depicts the Epanechnikov kernel density of the interest rate on low documentation loans in the year 2004 for two FICO groups620?(615619) and 620+(620624). The distribu- tions of interest rates observed in the two groups lie directly on topofoneanother.AKolmogorovSmirnovtestforequalityofdis- tribution functions cannot be rejected at the 1% level. Similarly, Figure IX.B depicts the density of LTV ratios on low documen- tationloansintheyear2004for620?and620+groups.Again, a KolmogorovSmirnov test for equality of distribution functions cannot be rejected at the 1% level. The fact that we find that the borrowers characteristics are similar around the threshold (Sec- tion IV.C) also confirms that selection based on observables is unlikely to explain our results.20

Second,theremightbeconcernsaboutselectionofloansby investors. In particular, our results could be explained if investors could potentially cherry pick better loans below the threshold. Theloanandborrowervariablesinourdataareidenticaltothe datauponwhichinvestorsbasetheirdecisions(Kornfeld2007). Furthermore, as shown in Section IV.C, these variables are smooth through the threshold, mitigating any concerns on selection by investors.21

Finally,strategicadverseselectiononthepartoflendersmay also be a concern. Lenders could, for instance, keep loans of better qualityontheirbalancesheetandofferonlyloansofworsequal- itytotheinvestors.Thisconcernismitigatedforseveralreasons.

- Theequalityofinterestratedistributionsalsorulesoutdifferencesintheexpected cost of capital across the threshold as an alternative explanation. Forinstance,lenderscouldoriginateriskierloansabovethethresholdonlybecausethe expected cost of capital was lower due to easier securitization. However, ina competitive market, the interest rates charged for these loans should reflectthe riskiness of the borrowers. In that case, as mean interest rates above andbelowthethresholdwouldbethesame(SectionC),lendersmusthaveaddedriskier borrowers above the thresholdresulting in a more dispersed interest ratedistribution above the threshold. Our analysis in Figure IX.A shows that this isnot the case.

- An argument might also be made that banks screen similarly aroundthe credit threshold but are able to sell portfolios of loans above and below thethresholdtoinvestorswithdifferentriskIfthiswerethecase,itcouldpotentiallyexplainourresultsinSectionIV.D.Thisdoesnotseemlikely.Becauseall the loans in our sample are securitized, our results on performance on loansaround the credit threshold areconditionalon securitization. Moreover, securitizedloans are sold to investors in pools that contain a mix of loans from the entire creditscorespectrum.Asaresult,itisdifficulttoarguethatloansof620?arepurchasedby different investors as compared to loans of 620+.

FigureIX

Dispersionof(A)InterestRatesand(B)Loan-to-Value(Low-Documentation)

The figure depicts the Epanechnikov kernel density of interest rate (A) andloan-to-value ratio (B) for two FICO groups for low-documentation loans620?(615619) as the solid line and 620+(620624) as the dashed line. The bandwidthfor the density estimation is selected using the plug-in formula of Sheather andJones (1991). The figures show that the densities of interest rates on loans aresimilarforboththegroups.AKolmogorovSmirnovtestforequalityofdistributionfunctions cannot be rejected at the 1% level. Data for loans originated in 2004 arereported here. We find similar patterns for 20012006 originations. We do notreport those graphs, for brevity.

First, the securitization guidelines suggest that lenders offer the entire pool of loans to investors and that conditional on observ- ables, SPVs largely follow a randomized selection rule to create bundles of loans. This suggests that securitized loans would look similar to those that remain on the balance sheet (Comptrollers Handbook1997; Gorton and Souleles 2006).22In addition, this selection, if at all present, will tend to be more severe below the credit threshold, thereby biasing us against finding any effect of screening on performance.

Weconductanadditionaltestthatalsosuggeststhatourre- sultsarenotdrivenbyselectiononthepartoflenders.Although banksmayscreenandthenstrategicallyholdloansontheirbal- ancesheets,independentlendersdonotkeepaportfolioofloans on their books. These lenders finance their operations entirely out of short-term warehouse lines of credit, have limited equity capital, and have no deposit base to absorb losses on loans that theyoriginate(Gramlich2007).Consequently,theyhavelimited motives for strategically choosing which loans to sell to investors. However,becauseloansbelowthethresholdaremoredifficultto securitizeandthusarelessliquid,theseindependentlendersstill have strong incentives to differentially screen these loans to avoid losses.Wefocusontheselenderstoisolatetheeffectsofscreening in our results on defaults (Section IV.D).

Totestthis,weclassifythelendersintotwocategoriesbanks (banks, subsidiaries, thrifts) and independentsand examine the performance results only for the sample of loans originated by independentlenders.Itisdifficulttoidentifyallthelendersin thedatabasebecausemanyofthelendernamesareabbrevi- ated.Inordertoensurethatweareabletocoveramajority ofoursample,weclassifythetopfiftylenders(byorigina-tionvolume)acrosstheyearsinoursampleperiod,basedonalistfromthepublicationInsideB&CMortgage.Inunre- portedresults,weconfirmthatindependentlendersalsofol- low the rule of thumb for low-documentation loans. Moreover, low-documentation loans securitized by independents with credit scores of620?are about 15% less likely to default after a year as

- We confirmed this fact by examining a subset of loans held on the lendersbalance sheets. The alternative data set covers the top ten servicers in the sub-primemarket(morethan60%ofthemarket)withdetailsonperformanceandloanterms of loans that are securitized or held on the lenders balance sheet. We findno differences in the performance of loans that are securitized relative to thosekept by lenders, around the 620 threshold. Results of this analysis are availableupon request.

compared to low-documentation loans securitized by them with credit scores 620+.23Note that the results in the sample of loans originated by lenders without a strategic selling motive are sim- ilar in magnitude to those in the overall sample (which includes other lenders that screen and then may strategically sell). This finding highlights that screening is the driving force behind our results.

- AdditionalVariationfromaNaturalExperiment

Unrelated Optimal Rule of Thumb.So far we have worked under the assumption that the 620 threshold is related to secu- ritization. One could plausibly argue, in the spirit of Baumol and Quandt (1964), that this rule of thumb could have been set by lenders as an optimal cutoff for screening that was unrelated to differential securitization. Ruling this alternative out requires an examination of the effects of the threshold when the ease of secu- ritization varies, everything else equal. To achieve this, we exploita natural experiment that involves the passage of antipredatory lending laws in two states which reduced securitization in the subprime market drastically. Subsequent to protests by market participants, the laws were substantially amended and the secu- ritization market reverted to prelaw levels. We use these laws to examine how the main effects vary with the time series variationin the ease of securitization likelihood around the threshold in the two states.

In October 2002, the Georgia Fair Lending Act (GFLA) went into effect, imposing antipredatory lending restrictions that atthe time were considered the toughest in the United States. The law allowed unlimited punitive damages when lenders did not comply with the provisions, and that liability extended to hold-ers in due course. Once GFLA was enacted, the market response was swift. Fitch, Moodys, and S&P were reluctant to rate securi- tized pools that included Georgia loans. In effect, the demand for the securitization of mortgage loans from Georgia fell drastically during the same period. In response to these actions, the Georgia legislature amended the GLFA in early 2003. The amendments removed many of the GFLAs ambiguities and eliminated covered loans.SubsequenttoApril2003,themarketrevivedinGeorgia.