Variance Analysis and Behavioural Implications in Cost Accounting ACC4025

- Subject Code :

ACC4025

Question 1

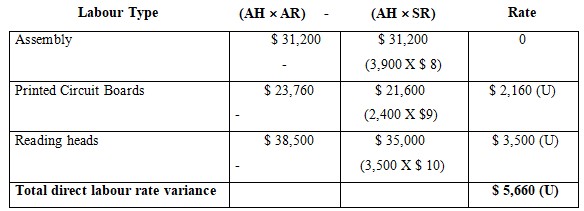

(a)Direct labour rate variance = (AH AR) (AH SR)

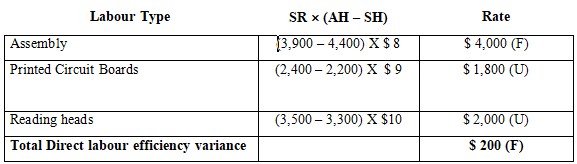

(b)Direct labour efficiency variance = (ActualHoursWorked ?StandardHoursAllowed) StandardRateperHour

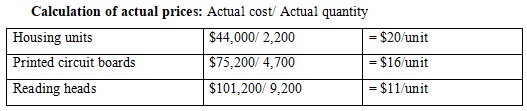

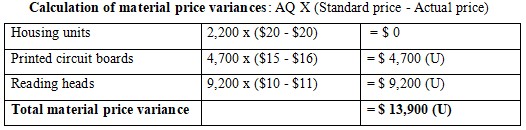

(c)Material price variance = Actual quantity x (Standard price - Actual price)

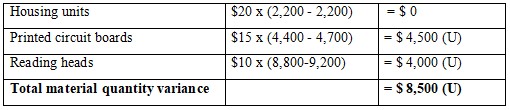

(d)Material quantity variance = Standard price x (Standard quantity - Actual quantity)

Calculation of standard quantity: Actual units x Standard quantity per unit

Calculation of material Quantity variances: Standard price x (Standard quantity - Actual quantity)

(e)Variable overhead spending variance = (Actual hours x Standard rate) - Actual variable overhead = (9,900 x $ 2) - $ 18,800 = $ 1,000 (F)

(f)Variable overhead efficiency variance = Standard rate x (Standard hours -Actual hours)

Standard hours: Actual units x Standard hours per unit = 2,200 x 4.5 hours per unit

= 9,900 hours

Variable overhead efficiency variance = $2 x (9,900 - 9,900) = $ 0

(g)SalesPriceVariance= (ActualSellingPrice?BudgetedSellingPrice) ActualUnitsSold SalesPriceVariance

= ($ 200?$ 200) 2,200 = 0

(h)SalesVolumeVariance=(ActualUnitsSold?BudgetedUnitsSold)BudgetedContrib-utionMarginperUnit

SalesVolumeVariance = (2,200?2,000) X ($122,000/2,000)

SalesVolumeVariance = 200 X 61 = $ 12,200 (F)

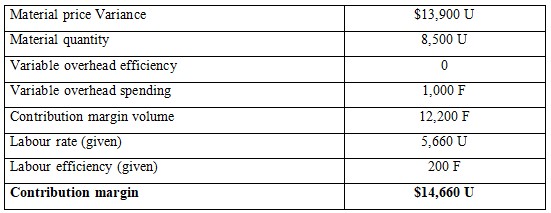

Reconciliation of contribution margin variance ($14,660 Unfavourable variance):-

The primary cause of the unfavourable contribution margin variance is an upsurge in direct labour & material costs. The advantages of raising revenue were mitigated by the unfavourable material price, quantity, & labour rate variations, notwithstanding the favourable sales volume variance. As a result, the overall contribution margin dropped & the total variable costs rose significantly.

2 (a) Behavioural factors that may promote friction among the production managers & between the production managers & the maintenance manager include:-

More Machine Downtime: The PCB & RH group managers felt annoyed with the maintenance manager because equipment kept breaking down. This meant workers had nothing to do & then had to work overtime, which made labor costs go up. This put even more stress on how they got along.

Production Pressure: The Assembly Group needs timely inputs from the PCB & RH groups to hit higher production goals. When the Assembly Group manager pushed to increase output, this pressure forced the PCB & RH groups to turn down parts instead of changing them. This created friction between these production managers.

2. (b) Jack Rath's analysis falls short & lacks depth. Rath noted the labor concerns, but he skipped over other crucial factors that lead to the unsatisfactory effects, which included material differences & maintenance challenges that brought about downtime. Rath's report might be seen by production teams to be partial & insufficient given that it focuses primarily on labor-related worries without considering the true causes or the broader context. This can cause the department managers to feel even less confident of their peers & even less satisfied.

Are you struggling to keep up with the demands of your academic journey? Don't worry, we've got your back!

Exam Question Bank is your trusted partner in achieving academic excellence for all kind of technical and non-technical subjects. Our comprehensive range of academic services is designed to cater to students at every level. Whether you're a high school student, a college undergraduate, or pursuing advanced studies, we have the expertise and resources to support you.

To connect with expert and ask your query click here Exam Question Bank